From 2022, Polish entrepreneurs can take advantage of the robotization relief – a solution that is intended to encourage the automation of processes (e.g. in production or logistics) and increase the attractiveness of enterprises on the domestic and foreign markets. We remind you what this preference is and what doubts it raises.

What is the robotization relief?

The robotization relief consists in an additional deduction from the tax base of 50% of the tax-deductible costs incurred for robotization (mainly the acquisition of new industrial robots, details below). This means that it is possible to reduce the tax base by 150% of the costs incurred for the purchase of the robot. The relief can be used by both: PIT taxpayers – natural persons and CIT – companies (Article 38eb of the CIT Act, Article 52jb of the PIT Act).

What costs are deductible?

Tax-deductible costs incurred for robotization in the years 2022-2026 are deductible. These include:

1.Costs of acquiring brand new ones:

-

- industrial robots,

- machines and peripherals for industrial robots functionally related to them,

- machines, devices and other things functionally related to industrial robots, used to ensure ergonomics and safety at work stations where there is interaction between humans and industrial robots, in particular sensors, controllers, relays, safety locks, physical barriers (fences, covers) or optoelectronic protective devices (light curtains, area scanners),

- machines, devices or systems used for remote management, diagnosis, monitoring or servicing of industrial robots, in particular sensors and cameras,

- human-machine interaction devices for industrial robots;

2. costs of acquisition of intangible assets necessary for the proper commissioning and acceptance for use of industrial robots and other fixed assets listed in point 1;

3. costs of acquisition of training services related to industrial robots and other fixed assets or intangible assets referred to in points 1 and 2;

4. lease payments for industrial works and other fixed assets listed in point 1 if, after the expiry of the basic term of the lease agreement, the financer transfers ownership of these fixed assets to the user.

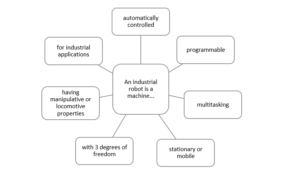

Definition of Industrial Robot

The relief is available if the purchased machine meets the definition of an industrial robot. An industrial robot is understood as a machine with strictly defined features, i.e.:

and which meets the following conditions in total:

- exchanges data in digital form with control and diagnostic or monitoring devices for remote control, programming, monitoring or diagnosis;

- it is connected to ICT systems improving the taxpayer’s production processes, in particular with production management, product planning or design systems;

- is monitored by sensors, cameras or other similar devices;

- is integrated with other machines in the taxpayer’s production cycle.

In order to consider a given machine as an industrial robot, it is necessary to meet all the above conditions. The Act additionally introduces the concept of machines and peripherals for industrial robots.

Settlement of the robotization relief

Taxpayers argue with tax offices about the method of deducting the costs incurred for robotization. The dispute concerns whether the following are deductible (in the amount of 50%):

A. depreciation write-offs on robots – this is the position of the tax authorities, or

B. actual expenses for the acquisition of works (i.e. a one-off deduction of the costs of purchasing the work in the year of incurring the expense) – this is most often the position of taxpayers.

Tax offices argue that 50% of “tax-deductible costs” are deductible, and the “tax-deductible costs” here is depreciation write-offs, not expenses for the purchase of the robot. Such an approach has been presented, eg. in individual tax rulings: of 3 September 2025, No. 0111-KDIB2-1.4010.295.2025.2.BJ, of 7 August 2025, No. 0114-KDIP2-1.4010.329.2025.2.KW, of 2 July 2025, No. 0111-KDIB2-1.4010.151.2025.2.ED.

However, this is not confirmed by case law. The courts indicate that the provisions on the relief introduce their own definition, indicating that “the costs of acquiring brand-new industrial robots are considered to be tax-deductible costs incurred for robotization.” Therefore, 50% of the expenses incurred for the purchase of robots are deductible. This was indicated, for example, in the judgments:

- The Provincial Administrative Court in Poznań of 10 June 2025 (ref. no. I SA/Po 167/25, not final),

- Provincial Administrative Court in Łódź of 9 January 2025 (ref. no. I SA/Łd 713/24, not final),

- Provincial Administrative Court in Warsaw of 21 December 2023 (ref. no. III SA/Wa 1993/23, not final).

The exception here is the negative judgment of the Provincial Administrative Court in Wrocław of 18 May 2023 (ref. no. I SA/Wr 947/22, legally binding).

To date, the correctness of the method of settling the relief has still not been resolved by the Supreme Administrative Court, and the lack of an unambiguous position of the Supreme Administrative Court further intensifies the uncertainty of taxpayers.

The use of robots – not only in industry

The regulations indicate that an industrial robot is understood as a machine for industrial applications. The tax authorities emphasize that this is only about the application to production understood as the production of goods. In the opinion of the tax authorities, it is therefore not possible to take advantage of the robotization relief in activities other than manufacturing, e.g. in trade or logistics. For example, rulings of 7 November 2025, no. 0111-KDIB2-1.4010.426.2025.1.ED, of 2 October 2025, no. 0111-KDIB2-1.4010.344.2025.1.ED.

In turn, the case-law emphasizes that the term “for industrial use” should not refer only to production. According to the courts, this concept should refer to the production of goods understood as the entire production process of the taxpayer, including other stages of production (e.g. packaging, storage). Nevertheless, according to the courts, the occurrence of any element of production is crucial. In the absence of it, it may be impossible to take advantage of the robotization relief. The inability to take advantage of the relief in the event of a lack of production activity is confirmed, for example, by the judgment of the Provincial Administrative Court in Łódź of 6 December 2023 (ref. no. I SA/Łd 801/23) and the Provincial Administrative Court in Poznań of 24 May 2023 (ref. no. I SA/Po 52/23)

Loss from business activity and deduction of relief

Finally, it is worth pointing out that the deduction is made in the tax return for the tax year in which the costs of robotization were incurred. If in a given year a loss was incurred or income was generated that is lower than the amount of the deductions entitled, the deduction – in the whole amount or in the remaining part, respectively – is made in the returns for the consecutive 6 consecutive tax years immediately following the year in which the deduction was used or the right to use the deduction existed.

ABC Tax Commentary

We are observing an increasing interest in robotization relief among our clients. Given the significant costs of robotization, this relief gives large tax savings. The doubts indicated above should in no case be an obstacle to taking advantage of the relief. It should be remembered that the relief can only be used until 2026 (although there were plans to extend it). If you had the opportunity to take advantage of the relief in previous years and did not do so, it is of course possible to use the relief retrospectively – to correct the tax return and claim the overpaid tax.